Big Tech's AI Infrastructure Bet Reaches a Scale That Rewrites the Playbook

Amazon, Meta, and Anthropic have collectively committed hundreds of billions to AI buildout — and a wave of earnings beats suggests the supply chain is already cashing in.

The Numbers That Reframe Everything

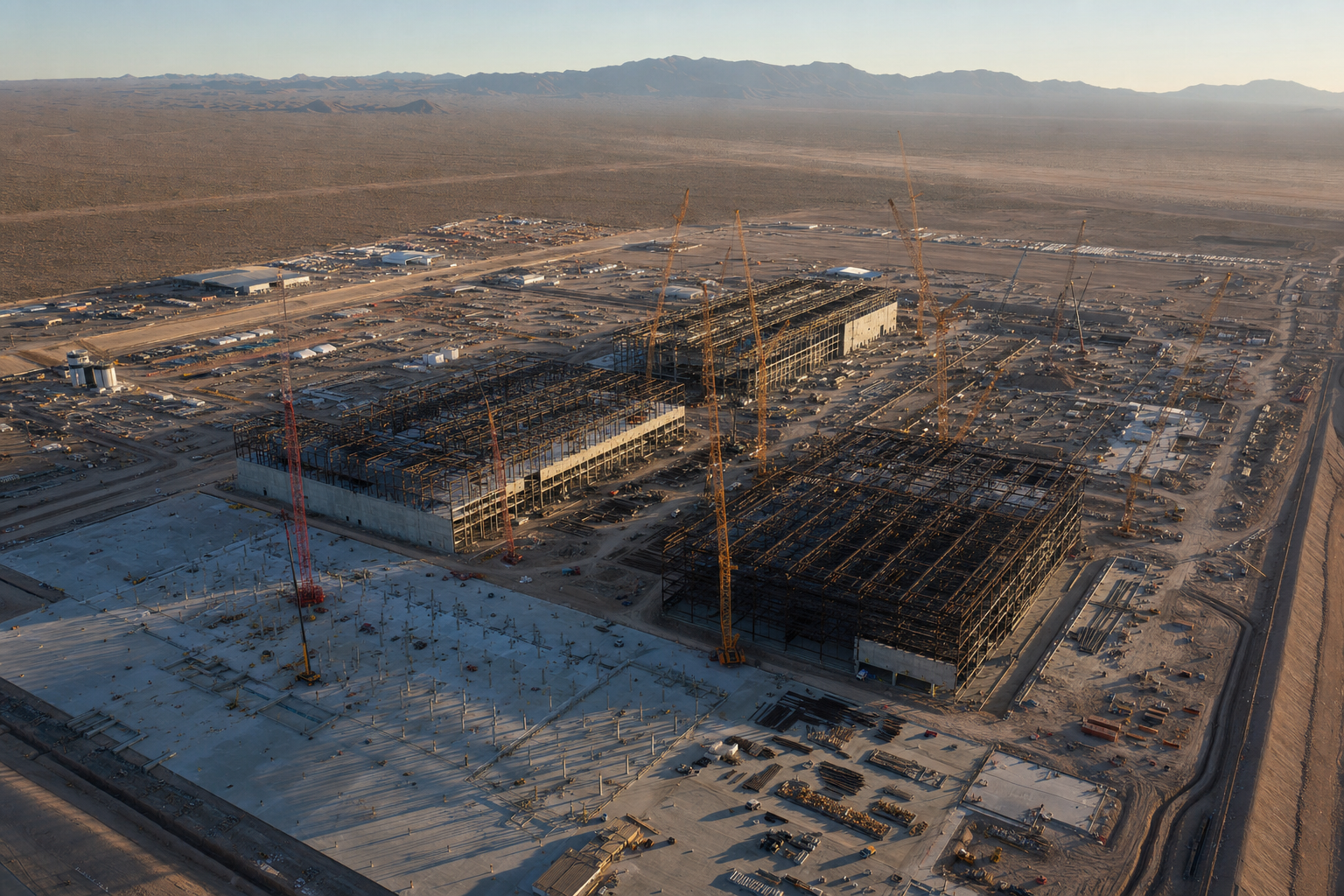

Spend enough time around technology stocks and you develop a tolerance for large numbers. But the AI infrastructure commitments that landed this week are different in kind, not just degree.

Amazon (AMZN) CEO Andy Jassy announced $200 billion in capital expenditures for 2026 — described as the largest single-year infrastructure investment in corporate history. Meta Platforms (META) outlined plans to invest up to $145 billion in AI infrastructure, a figure it disclosed alongside a first-quarter earnings report that beat Wall Street's earnings-per-share expectations by a significant margin. And Anthropic, the AI safety company, committed to spend approximately $200 billion on Alphabet's (GOOGL) Google Cloud over five years — a deal that cements Alphabet as a structural beneficiary of the AI buildout regardless of how the competitive landscape among AI labs evolves.

These are not projections or aspirational targets. They are capital commitments from companies with the balance sheets to honor them. Taken together, they represent a bet that AI infrastructure is a long-cycle investment with durable returns — and that the window to secure capacity is now.

The Earnings Cycle Is Validating the Thesis

What makes this moment distinct from earlier phases of the AI hype cycle is that the spending is now showing up in reported revenue, not just forward guidance.

Apple (AAPL) posted its best March quarter on record: $111.18 billion in revenue and $29.58 billion in net income. The company paired those results with a $100 billion share repurchase program and a 4% dividend increase — a capital allocation posture that stands in deliberate contrast to peers racing to build data centers. Apple's strategy of generating strong cash flows while others absorb the upfront costs of AI infrastructure has drawn analyst attention as a potentially underappreciated position.

Advanced Micro Devices (AMD) beat first-quarter estimates and issued second-quarter guidance above consensus, triggering a broad round of upward price target revisions. Arm Holdings (ARM) separately forecast first-quarter revenue of $1.26 billion — above analyst estimates — citing surging adoption of its chip architecture in AI data centers. The two reports, arriving in close proximity, reinforce a pattern that has been building across the semiconductor sector: AI infrastructure demand is outpacing earlier projections, and multiple companies in the supply chain are capturing that upside simultaneously.

Amazon logged its fifth consecutive quarter of beating Wall Street's earnings-per-share expectations. Sixty of 65 analysts covering the stock rate it a buy, with none recommending a sell — a degree of consensus that is itself a data point about how the market is pricing AI infrastructure exposure.

Where the Money Actually Flows

Understanding the investment implications requires tracing how infrastructure spending moves through the supply chain.

At the top of the stack sit the hyperscalers — Amazon, Meta, Alphabet, and Microsoft — committing the capital. Below them are the chip designers: Nvidia (NVDA), AMD, and Arm, whose processors and architectures power AI training and inference workloads. Further down are the companies supplying the physical infrastructure those chips require.

Nvidia's 5% share price gain this week followed the announcement of a multiyear supply and technology partnership with Corning (GLW) focused on optical connectivity for AI data centers. The deal is valued at $500 million and includes plans to establish new fiber optics manufacturing plants in the United States. Corning's stock surged 14% on the news, and the company raised its long-term sales targets.

Optical connectivity — fiber-based data transmission that moves information between chips and servers at high speed and low latency — has emerged as a bottleneck as data center scale expands. The Nvidia-Corning deal is a direct response to that constraint: locking in domestic optical capacity reduces exposure to supply disruptions as hyperscalers accelerate construction timelines.

The Pentagon's $500 million contract awarded to Scale AI — an AI data-labeling and analytics company backed by Meta — adds another dimension. Government appetite for commercial AI capabilities is growing, and Scale AI's defense contract signals that the addressable market for AI infrastructure extends beyond the private sector. Meta's backing gives it indirect exposure to that revenue stream.

Apple's Contrarian Posture

Amid the spending frenzy, Apple's approach deserves separate attention. While peers are committing hundreds of billions to data center construction, Apple posted record cash generation and immediately returned capital to shareholders. The $100 billion buyback is one of the largest in corporate history.

Reports also suggest Apple is in talks to use Intel (INTC) and Samsung as U.S.-based chip suppliers — a potential manufacturing realignment that neither company has publicly confirmed, but which analysts are watching as a consequential supply chain story. If confirmed, it would mark a significant shift away from Apple's long-standing reliance on Taiwan Semiconductor Manufacturing Company and could become one of the more strategically important domestic manufacturing decisions of the current trade policy era.

Apple's financial position gives it the flexibility to absorb the cost premiums typically associated with domestic chip production. Whether it chooses to do so at scale will be a defining question for the company's supply chain strategy over the next several years.

What the Spending Scale Actually Means

The sheer volume of capital being committed raises a question that investors are right to hold onto: when does this translate into returns?

Capital expenditure of this magnitude typically takes years to generate revenue. Data centers take time to build, commission, and fill with workloads. The Anthropic-Google Cloud deal, for instance, unfolds over five years — meaning the $200 billion in commitments will flow gradually, not immediately. Amazon's $200 billion in 2026 capex will depreciate over the useful life of the assets, creating a sustained drag on free cash flow even as revenue grows.

The bull case is straightforward: AI demand is growing faster than supply, and the companies building infrastructure now are securing competitive advantages that will be difficult to replicate later. The 60-of-65 analyst buy rating on Amazon reflects that view.

The bear case is less about the technology and more about the timing. If AI adoption among enterprise customers scales more slowly than hyperscaler investment assumptions imply, the return on these commitments could disappoint. The market is currently pricing in the bull case across most of the supply chain — which means any guidance revision that suggests demand is plateauing would carry outsized downside.

What to Watch

The most important forward signal is not another earnings beat — it's whether guidance language from hyperscalers starts to shift. Any commentary suggesting data center utilization rates are not meeting expectations, or that enterprise AI adoption is slower than projected, would challenge the thesis that underpins the current valuations across the sector.

The SOXX, SMH, and FTXL semiconductor ETFs have reflected the current strength. Their behavior on any macro or guidance disappointment will indicate how much risk premium the market has already priced in.

The Apple-Intel chip sourcing talks, if confirmed, could reshape domestic semiconductor manufacturing economics in ways that extend well beyond Apple's own supply chain. And the Anthropic-Google Cloud commitment will be worth revisiting when Alphabet reports cloud revenue — it should eventually show up as a durable revenue anchor in the numbers.

For now, the AI infrastructure buildout is producing a rare alignment: massive capital commitments, earnings beats across the supply chain, and analyst consensus pointing in one direction. That alignment won't last indefinitely. The question is whether the underlying demand justifies it before the cycle turns.