April Core PCE Holds at 3.3% YoY; MoM Print Cools to 0.2%

The Fed's preferred inflation gauge matched annual forecasts but came in softer than expected on a monthly basis, offering modest relief ahead of the next FOMC decision.

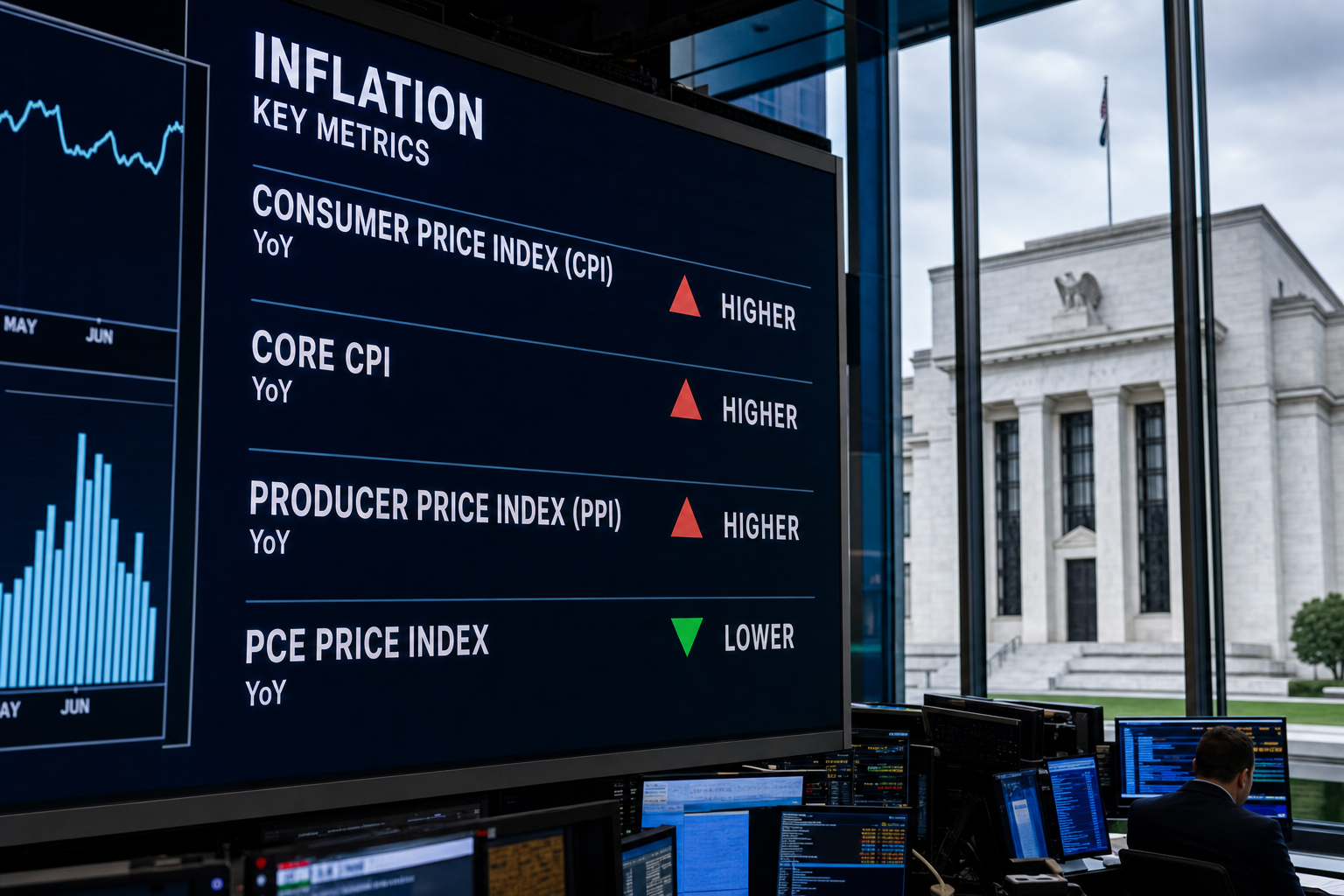

Core PCE Meets Annual Target, Monthly Reading Undershoots

The U.S. Bureau of Economic Analysis reported Thursday that the Core Personal Consumption Expenditures (PCE) price index rose 3.3% year-over-year in April 2026, exactly in line with consensus estimates. On a monthly basis, however, the gauge posted a 0.2% gain, coming in one tenth of a percentage point below the 0.3% forecast — a modest but notable softening that markets will scrutinize closely.

Core PCE, which strips out volatile food and energy components, is the Federal Reserve's preferred measure of underlying inflation. The data point carries outsized weight in shaping monetary policy expectations, particularly as the Fed navigates the final stretch of its disinflation campaign.

What the Numbers Mean

The in-line annual reading confirms that inflation remains above the Fed's 2% long-run target, but the softer monthly print suggests price pressures are not re-accelerating — a key concern that had rattled markets in recent months. A monthly reading of 0.2% annualizes to roughly 2.4%, which, if sustained, would represent meaningful progress toward the Fed's objective.

Personal income and personal consumption data released alongside the PCE figures will also be parsed by traders for signals on consumer resilience. Strong consumption paired with cooling inflation would represent a so-called "soft landing" dynamic, while any signs of demand deterioration could complicate the policy calculus.

Fed Policy Implications

With the Federal Open Market Committee's next scheduled meeting on June 17–18, 2026, today's data arrives at a critical juncture. Fed officials have repeatedly signaled they require sustained evidence of disinflation before resuming rate cuts. The April Core PCE print does not, on its own, clear that bar — but the softer monthly figure reduces the probability of a hawkish surprise at the upcoming meeting.

Fed funds futures markets will likely reprice modestly following the release. Prior to the data, traders had assigned a low probability to a June cut, with the first fully priced reduction expected later in the year. A 0.2% monthly print may nudge those expectations slightly earlier, though a single data point is unlikely to trigger a decisive shift in Fed communication.

Market Context

Equity markets had been on edge ahead of the release, with the S&P 500 sensitive to any upside inflation surprise that could push rate-cut expectations further into 2027. Treasury yields across the curve had reflected cautious positioning. The softer-than-expected monthly reading may provide near-term relief for rate-sensitive sectors including real estate, utilities, and growth-oriented technology stocks.

For fixed income investors, the data supports a modestly constructive view on duration. If subsequent months confirm the 0.2% monthly trend, the cumulative disinflationary signal would strengthen the case for the Fed to begin easing before year-end.

Key Figures at a Glance

- Core PCE YoY (April): 3.3% — in line with 3.3% estimate

- Core PCE MoM (April): 0.2% — below 0.3% estimate

- Fed Target: 2.0% (long-run)

- Next FOMC Meeting: June 17–18, 2026

Investors will now turn attention to the May employment report and upcoming CPI data to assess whether April's softer monthly print marks the beginning of a renewed disinflationary trend or a temporary fluctuation.